When investors talk about Bitcoin mining companies, they are no longer just talking about who owns the most machines. In March 2026, the market cares about three things at once: scale, fleet efficiency, and whether a miner can turn power-rich sites into AI and high-performance computing capacity. That is why the old screening method for top Bitcoin mining companies feels outdated. If you are comparing a Bitcoin mining company, the modern checklist is EH/s, J/TH, cost to mine one BTC, access to curtailed or low-cost power, and the company’s ability to monetize infrastructure beyond pure mining.

For readers searching the top 10 Bitcoin mining companies, the largest Bitcoin mining companies, or the biggest Bitcoin mining companies, the real takeaway is that today’s winners look more like digital-infrastructure operators than old-school commodity miners. The best-run names now sit at the intersection of Bitcoin, power markets, cooling design, and AI data-center leasing. That shift is what separates speculative crypto mining companies from the crypto mining companies to invest in.

The State of Public Bitcoin Mining: March 2026 Market Analysis

How the Top Miners Adapted to Lower Block Rewards

The April 2024 halving did exactly what many expected: it split the public-mining field into survivors and strugglers. Riot said its average cost to mine one Bitcoin, excluding depreciation, rose to $49,645 in 2025 from $32,216 in 2024, while Core Scientific reported a cash cost to self-mine one Bitcoin of $56,627 in Q1 2025. TeraWulf’s year-to-date September 2025 cash cost to mine one Bitcoin was $51,523. In other words, scale alone did not save anyone; the post-halving survivors were the ones that improved efficiency, monetized power flexibility, or added new revenue streams.

That is why many of the largest Bitcoin miners now look more disciplined than aggressive. Instead of chasing raw fleet growth at any cost, they are pruning older rigs, leaning on demand response, and redirecting capital into higher-return infrastructure. The new benchmark for top Bitcoin miners is not “Who can shout the biggest EH/s number?” It is “Who can keep margins alive when network difficulty rises and block rewards stay lower?”

Why Bitcoin Miners are Now High-Performance Computing (HPC) Giants

The AI-HPC pivot is the most important 2026 trend that many older articles miss. MARA announced a strategic agreement with Starwood to develop AI and HPC infrastructure on select power-rich sites and also completed the acquisition of a controlling interest in Exaion, expanding its AI and secure cloud capabilities. Riot now frames itself as a builder of large-scale data centers, not just a miner, and has already begun generating revenue from its AMD lease at Rockdale. CleanSpark explicitly told investors it is “no longer a single-track business,” while TeraWulf said HPC hosting became its primary growth engine in 2025.

Core Scientific may be the clearest proof that the pivot is real, not promotional. By March 2026 it had energized about 350 MW for CoreWeave and said it remained on track to deliver about 590 MW by early 2027. That is why the market now values some Bitcoin mining public companies less like pure BTC proxies and more like hybrid infrastructure plays with optionality across mining, colocation, and AI workloads.

Energy Strategy: The Shift Toward 100% Sustainable and Curtailed Power

Energy strategy has become just as important as miner procurement. Cambridge said sustainable energy sources now account for 52.4% of Bitcoin mining’s energy use, with natural gas replacing coal as the single largest source. Public miners have adapted by blending demand response, grid balancing, hydro, stranded gas, and low-carbon sourcing instead of depending on a single power story.

You can see that shift in company disclosures. Riot’s operating model in Texas still benefits from curtailment and power credits, CleanSpark says its data centers primarily run on low-carbon power, and MARA continues to frame its energy thesis around clean, stranded, or otherwise underutilized energy, including its hydro-powered Paraguay project. Among Bitcoin mining companies in the USA, this power-market sophistication now matters as much as ASIC selection.

Top 5 Public Bitcoin Mining Companies

The snapshot below uses each company’s latest official operating disclosures together with March 2026 market data. Because miners report “current hashrate” differently, some figures reflect operational or deployed capacity rather than pure self-mining output.

| Company | Ticker | Current Hashrate (EH/s) | Energy Source |

| Marathon Digital Holdings | MARA | 66.4 | Mixed portfolio: grid, underutilized energy, flare gas, hydro JV |

| Riot Platforms | RIOT | 38.5 | ERCOT-linked grid power with curtailment and demand response |

| CleanSpark | CLSK | 50.0 | Primarily low-carbon power |

| Core Scientific | CORZ | 20.1 | Grid-connected data centers with flexible power management |

| TeraWulf | WULF | 8.5 | Low-carbon infrastructure with sustainable-power focus |

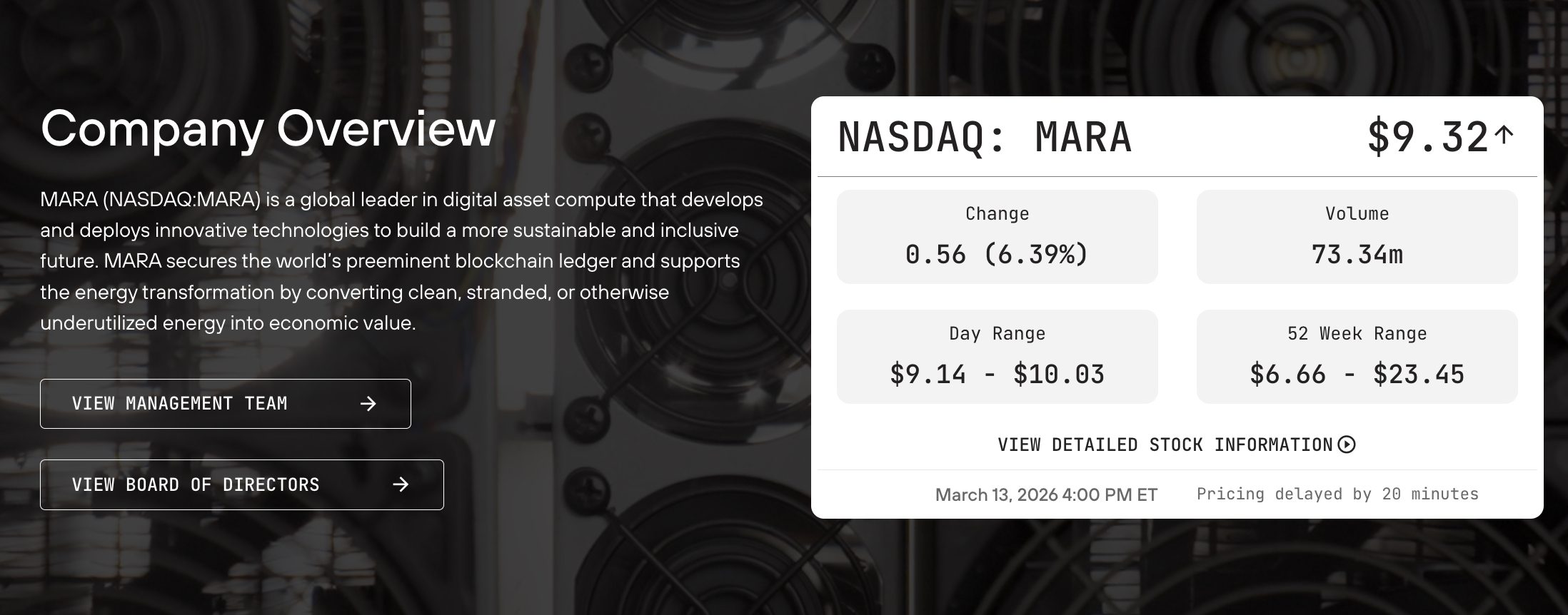

Marathon Digital Holdings (MARA): The Global Fleet Leader

Source: MARA

MARA remains the fleet-scale reference point. Its fourth-quarter 2025 shareholder letter reported 66.4 EH/s of energized hashrate, and its September 2025 materials said current energy efficiency had improved to 18.6 J/TH. That combination still makes MARA one of the largest and most closely watched names in the public-miner universe, even though its March 2026 market cap is smaller than some newer infrastructure darlings.

What makes MARA more interesting in 2026 is international and infrastructural reach. Between the hydro-powered Paraguay joint venture, the Kenya energy-sector partnership, and the Exaion transaction in France, MARA is building a broader digital-compute footprint than the average Bitcoin miner company. That global posture, combined with the Starwood AI/HPC joint venture, gives it a bigger strategic canvas than simple BTC production numbers suggest.

Riot Platforms (RIOT): Vertically Integrated Powerhouse in Texas

Source: Riot

Riot’s bull case is still vertical integration plus power access. Its December 2025 update showed 38.5 EH/s of deployed hash rate and 20.2 J/TH fleet efficiency, while its March 2026 earnings release highlighted record annual revenue, 5,686 Bitcoin mined, and rising monetization of its data-center assets. Riot is one of the clearest examples of how BTC mining companies are becoming power-and-land platforms first and mining fleets second.

The fresh 2026 angle is Texas optionality. Riot’s January 2026 announcement said Rockdale and Corsicana together represent 1.7 GW of fully approved power capacity, and the AMD lease at Rockdale is already operational. So even if Bitcoin mining remains core, Riot increasingly looks like a digital-infrastructure landlord with one of the deepest Texas power portfolios in the sector.

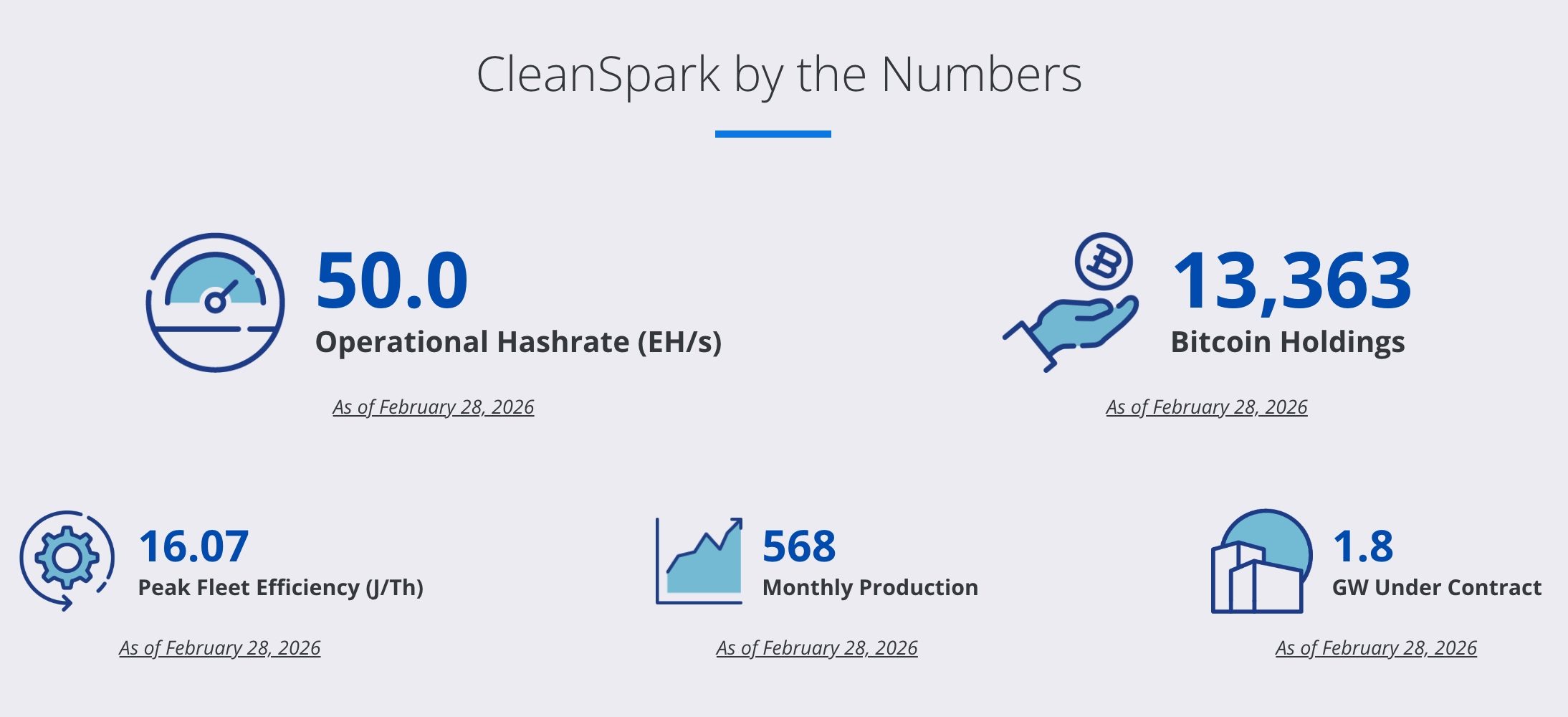

CleanSpark (CLSK): The “Efficiency King” of the 2025–2026 Cycle

Source: CleanSpark

If one company owns the “efficiency” label, it is CleanSpark. Its February 2026 operating update reported 50.0 EH/s operational hashrate, 43.2 EH/s average operating hashrate, and a peak deployed-fleet efficiency of 16.07 J/TH. That is elite by public-miner standards and a big reason many investors treat CLSK as the cleanest operational execution story among the current largest crypto mining companies.

CleanSpark’s 2026 twist is that it is using that mining engine to fund AI-ready site expansion. In February 2026 the company said it had secured up to 890 MW of new utility-grade power capacity and was advancing a multi-gigawatt AI infrastructure platform. That means CleanSpark is no longer just a lean miner; it is trying to become one of the more credible crypto mining companies to invest in for investors who want both BTC exposure and AI optionality.

Core Scientific (CORZ): The Comeback Story and AI Data Center Leader

Source: Core Scientific

Core Scientific’s turnaround story is no longer theoretical. By year-end 2025 it was running about 19.1 EH/s of self-mining and 1.0 EH/s of hosted capacity, and its average self-mining fleet efficiency had improved materially from earlier years. Its March 2026 results also emphasized continued execution on the CoreWeave contract, with roughly 350 MW already energized.

Among all the largest Bitcoin mining companies, Core may have the clearest AI monetization case today. The company’s multiyear CoreWeave relationship grew from an initial HPC agreement into a total contracted footprint of roughly 590 MW across six sites, and earlier disclosures put cumulative projected revenue from those CoreWeave contracts at up to $8.7 billion. That is why CORZ now trades less like a simple miner and more like a bridge asset between Bitcoin infrastructure and AI colocation.

TeraWulf (WULF): Pioneering Nuclear-Powered Mining and Low-Cost Production

Source: TeraWulf

TeraWulf’s mining story is a little different because its valuation has started to reflect HPC ambitions as much as BTC output. As of September 30, 2025, it reported 8.5 EH/s of operational hashrate and an average miner efficiency of 17.5 J/TH, while its March 2026-era market cap sat above several better-known miners. That looks surprising until you realize the market is pricing TeraWulf more as a power-and-AI buildout story than a pure hashrate story.

The brand still benefits from the company’s nuclear-powered legacy at Nautilus and its broader low-carbon positioning, but the real 2026 driver is HPC leasing. TeraWulf said it entered 2026 with 522 critical IT MW under contract, over $12.8 billion of revenue tied to those contracts, and a 2.9-GW multi-regional platform. In that context, lower mining EH/s is not necessarily bearish; it reflects capital being redirected toward what management believes is the higher-multiple business.

Key Performance Indicators (KPIs)

Cost to Mine 1 BTC: Analyzing Operational Efficiency (OpEx)

The first KPI is still the simplest: what does it cost a company to produce one Bitcoin? Riot’s 2025 average cost to mine one Bitcoin, excluding depreciation, was $49,645. Core Scientific reported a 2024 total cost to self-mine one Bitcoin of $30,387, but that jumped to $56,627 in Q1 2025. TeraWulf’s year-to-date September 2025 cost to mine one Bitcoin was $51,523. Those numbers show why investors should never look at BTC price alone when evaluating Bitcoin mining companies.

Fleet Efficiency (J/TH): The Importance of Next-Gen ASIC Hardware

J/TH is now the most important technical metric after cost to mine. CleanSpark’s 16.07 J/TH is the standout number in this group. MARA disclosed 18.6 J/TH as of September 2025, Riot reported 20.2 J/TH in December 2025, Core Scientific was roughly mid-20s, and TeraWulf reported 17.5 J/TH as of September 2025. In a post-halving world, a few joules per terahash can mean the difference between positive cash flow and forced curtailment.

Exahash Growth (EH/s): Tracking Realized vs. Projected Hashrate

Exahash growth still matters, but investors should separate realized output from aspirational slide-deck numbers. CleanSpark’s 50 EH/s and MARA’s 66.4 EH/s show what scaled execution looks like. Riot’s 38.5 EH/s also matters because it is tied to a large approved power base. By contrast, companies shifting capacity into AI or HPC may show flatter mining growth even while enterprise value improves. That is why 2026 investors should read EH/s and infrastructure conversion together, not in isolation.

Mining Companies as AI Data Centers

Why Bitcoin Mining Sites are Perfect for AI Training

Bitcoin mining sites already solve several hard infrastructure problems: large power interconnects, industrial land, cooling design, high-load electrical systems, and in some cases water and fiber access. Riot’s Rockdale site, for example, now fully owned by the company, includes a 700 MW grid interconnection, dedicated water supply, and fiber connectivity. Those are exactly the ingredients hyperscalers and AI tenants care about.

Revenue Diversification

BTC mining revenue is volatile by nature; AI colocation revenue is usually contract-based and dollar-denominated. That difference is why miners are pivoting. CleanSpark told investors Bitcoin mining now generates the cash flow while AI infrastructure monetizes assets over the long term. TeraWulf said HPC hosting became its primary growth engine, and Core Scientific has repeatedly emphasized contracted revenue visibility through CoreWeave.

Case Study: Core Scientific’s Multi-Billion Dollar Deal with AI Providers

Core Scientific is the case study every investor should understand. Its CoreWeave relationship expanded through multiple agreements, with the company saying the total contracted HPC footprint had grown to about 590 MW across six sites. Earlier official releases said projected cumulative revenue associated with these contracts could reach $8.7 billion over time. That is a different earnings model from traditional mining, and it helps explain why some public miners no longer trade like simple leveraged BTC bets.

Regional Dominance: The Global Map of Bitcoin Mining

The United States: The Undisputed Hashrate Capital

The United States remains the center of gravity for industrial mining. Cambridge’s mining map continues to position the U.S. as the dominant jurisdiction for large-scale activity, and the public-market leaders in this article are overwhelmingly U.S.-listed and U.S.-operated. Texas in particular keeps showing up because of ERCOT flexibility, fast development timelines, and massive power availability.

The Latin American Expansion: Paraguay and El Salvador’s Growing Roles

Latin America matters for two different reasons. Paraguay matters economically because hydro power keeps attracting miners, including MARA’s hydro-powered project near Itaipu. El Salvador matters symbolically because sovereign Bitcoin policy and geothermal-mining narratives keep it central to the long-term conversation about state-backed mining, even if it is still far smaller than the U.S. industrial base.

The Resurgence of Central Asia: Navigating Energy Regulations in 2026

Central Asia, especially Kazakhstan, still matters, but the story is no longer about unregulated expansion. Early-2026 reporting says Kazakhstan continues tightening its legal framework, with licensed exchanges and mining compliance becoming more central to the market structure. For miners, that means the region may still be relevant, but only for operators comfortable with regulatory complexity and evolving energy-policy rules.

Investment Risks: Navigating the Volatility

Why Mining Stocks Don’t Always Follow BTC Price

Mining stocks often move like leveraged Bitcoin, but not always. The gap appears when financing risk, power costs, or AI execution matters more than BTC spot. A miner can underperform Bitcoin even in a bull market if its cost per coin rises too fast or if dilution fears overwhelm the benefit of higher BTC prices. That is why the best Bitcoin mining public companies are not always the best-performing mining stocks in a given quarter.

Understanding How Companies Fund Fleet Upgrades

Capital structure still matters. MARA has repeatedly used convertible notes; Riot sold Bitcoin to fund the Rockdale land acquisition; Core Scientific and TeraWulf have both leaned on large financing packages to support infrastructure expansion. That can create long-term value, but it can also dilute equity holders or change the risk profile if markets turn.

Tax Proposals and Environmental Legislation in 2026

Regulation remains a live risk even without a single dominant federal rule. Company filings continue to warn about permitting delays, power-market changes, and new laws or regulations affecting digital infrastructure, mining, and data-center development. For investors, that means Bitcoin mining companies in USA still carry political and environmental-policy risk on top of ordinary commodity-cycle risk.

The Future of Mining: What to Expect Through 2030

Consolidations and Mergers: Will We See a “Big Three” of Mining?

Consolidation looks more likely than fragmentation. As an inference from current filings and capital needs, the sector is drifting toward a smaller number of power-rich operators that can fund both ASIC refreshes and HPC buildouts. If that happens, the future leaders may come from today’s largest Bitcoin mining companies, but they will likely win because of land, substations, and long-term contracts, not just BTC treasury size.

Hardware Evolution: The Next Generation of Water-Cooled ASICs

Another reasonable inference is that liquid and water-cooled ASIC deployments will become more common. As miners chase lower J/TH and higher rack density while also preparing sites for AI workloads, thermal design becomes a competitive advantage. MARA has already tied efficiency gains to newer S21 deployments and immersion cooling, which points to where the next hardware wave is heading.

Sovereign Mining: When Will Nation States Start Mining Publicly?

Sovereign mining is still early, but the concept is no longer fringe. El Salvador’s ongoing BTC accumulation and domestic mining activity, combined with wider discussion of state-linked mining in places with cheap stranded power, suggest the idea has moved from theory to policy experiment. Publicly listed miners will likely be the first technical partners if more nation-states choose to formalize mining strategies.

FAQ: Critical Questions for Mining Stock Investors

Which Bitcoin mining company has the lowest production cost?

There is no single permanent winner, because companies report cost differently and the number changes with power prices and network difficulty. Based on recent disclosures, Riot and TeraWulf remain competitive on production economics, while CleanSpark stands out on fleet efficiency. In practice, investors should compare cost to mine one BTC and J/TH together, not separately.

Is it better to buy Bitcoin or Bitcoin mining stocks?

Buying Bitcoin is the cleaner macro bet. Mining stocks add operational leverage, management execution risk, financing risk, and power-market risk. That extra risk can outperform in strong cycles, but it can also underperform badly. If you want simple BTC exposure, buy BTC; if you want higher beta and believe in infrastructure execution, then selected top Bitcoin mining companies may make sense.

What does “Exahash” mean in a company’s financial report?

Exahash per second, or EH/s, measures mining compute power. One EH/s equals one quintillion hashes per second. In practice, it tells you how much Bitcoin-security work a miner can perform, but not whether that work is profitable. That is why EH/s must always be read alongside J/TH and cost per mined coin.

How does the halving affect public mining companies’ stock prices?

The halving reduces block rewards, which pressures margins immediately. After that, stock prices depend on who can offset the hit through better efficiency, cheaper power, treasury strategy, or AI/HPC diversification. The companies that adapted best after the 2024 halving were not just the ones with more rigs; they were the ones with better power economics and a believable second revenue engine.