If you’ve been searching for what is AMP token, you’ve come to the right place. AMP is still closely tied to payments, but in 2026 it makes more sense to think of it as a collateral layer rather than just a payment coin. Its job is not simply to move value. Its job is to stand behind value transfers and make them feel final before the underlying asset fully settles.

Why AMP is More Than Just a Payment Token in 2026

The Core Mission: Instant, Verifiable, and Fraud-Proof Asset Transfers

AMP’s mission has never been “be money.” Its mission is to help money move. The official docs define AMP as a universal collateral token that can guarantee transfers instantly while the underlying asset settles in the background. That is a very different value proposition from a simple payments coin. Instead of replacing every asset, AMP price stands behind many assets.

That distinction matters. In the AMP model, the merchant or counterparty does not need to wait for the base chain to reach full confidence before acting. The collateral sits in escrow under programmable rules, so settlement assurance becomes a product of smart-contract design rather than blind trust in timing. That is why AMP crypto still has a defensible niche in 2026.

From Flexa to Ampera: The Evolution of the Ecosystem

Flexa remains the most visible real-world use case, but 2025’s Capacity v3 migration moved Flexa’s collateral layer onto infrastructure “powered by Anvil and Alchemy,” making the architecture more modular and more obviously extensible than the old v2 design.

At the same time, Anvil introduced a separate onchain system for fully secured credit, vault-based collateral, and letters of credit governed by ANVL. That split is the key ecosystem transition: AMP continues as productive collateral for payment assurance, while Anvil expands the collateral thesis into broader finance.

AMP in 2026: Its Role in a Multi-Chain Financial Landscape

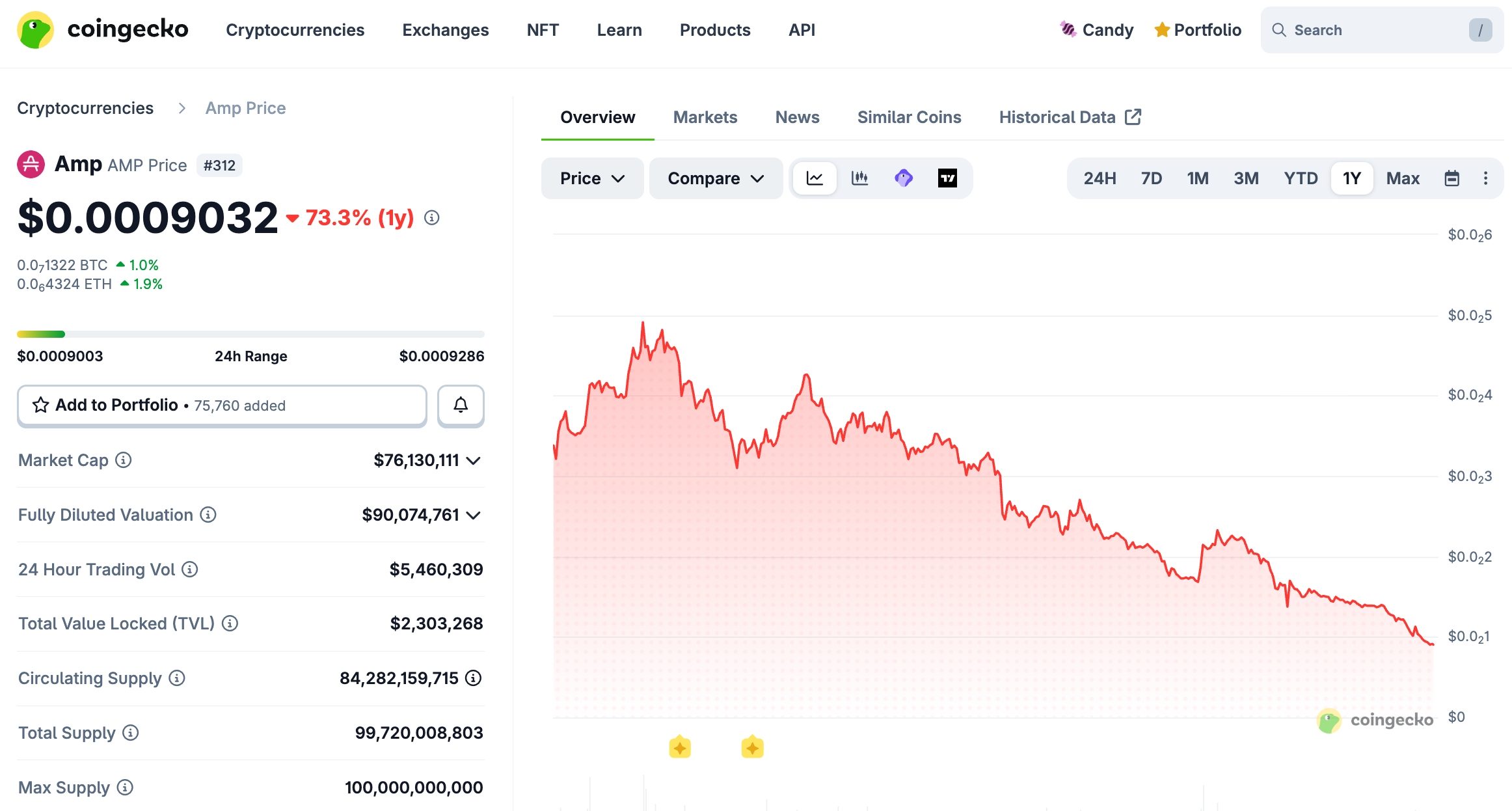

Source: CoinGecko

Flexa now positions itself as a platform for omnichannel digital-asset payments, with support for 99+ digital assets and SDK-based wallet integrations. Its Components toolkit supports networks including Base, Bitcoin, Ethereum, Lightning, Litecoin, Polygon, Solana, and Zcash. That makes AMP less like a single-chain bet and more like a neutral collateral layer sitting under many front-end payment experiences.

How AMP Works: The Power of Collateral Partitioning

Understanding “Collateral Managers”: The Smart Contracts Behind the Scenes

The most overlooked part of the AMP story is not staking. It is partitioning. AMP’s docs describe collateral managers as customizable smart contracts that can lock, release, and manage collateral under different rules for different use cases. Instead of one monolithic collateral pool, AMP lets those managers work over specific token partitions.

In practical terms, one Ethereum address can hold several “buckets” of AMP at once. The default bucket behaves like a normal ERC-20 balance. Other buckets are partition balances tied to special rules. The API exposes this directly through functions like balanceOfByPartition, partitionsOf, and transferByPartition.

The Mechanics of a Transaction: How AMP Assures Instant Settlements

A normal AMP-backed flow looks like this: a user initiates a transfer, a collateral manager escrows AMP immediately, the recipient gets assurance right away, and once the underlying transfer settles, the escrowed AMP is released for reuse. This is why Flexa can promise instant authorization even when the source asset itself may not have reached final settlement yet.

Here is where partition math becomes important. In the whitepaper’s example, a collateral manager controls 300 AMP across two delegated partitions, while users still retain portions of their balances elsewhere. After reward transfers, the manager-controlled amount rises to 400 AMP, but total token supply does not change; balances are simply redistributed across partitions. In plain English: partitioning lets AMP be productive without forcing a holder to surrender the entire wallet balance to a separate contract. That “stake-in-place” design is one of AMP’s smartest technical differentiators.

Even more interesting, the partition namespace is structured. The whitepaper explains that the first 4 bytes act as a partition prefix, while additional bytes can encode sub-partitions and a collateral-manager address. Under the distinct-partition validator, a single manager can control up to 2^64 sub-partitions inside its owned space. That gives institutions and apps a way to isolate risk by customer, app, asset class, or transaction type while keeping all of it inside the same token contract.

Fraud Protection: What Happens When a Payment Fails?

AMP’s protection model is simple in concept: successful settlements release collateral; unsuccessful or unauthorized outcomes do not automatically get that collateral back. Because managers can restrict transfers and redirect collateral according to their rules, the system turns uncertain settlement into pre-funded assurance. That is how Flexa can market complete fraud resistance and no chargebacks to merchants.

The Ampera Foundation and the Anvil Protocol (ANVIL)

The Relationship Between AMP and ANVIL

Anvil is not a rebrand of AMP. It is a separate protocol layer. Official Anvil docs describe it as a system of Ethereum smart contracts for managing collateral and issuing fully secured credit, with ANVL governing protocol operations through OpenZeppelin-based governor contracts. AMP, by contrast, remains the neutral collateral asset used in Flexa Capacity v3.

So the clean mental model is this: AMP is the collateral engine; ANVL is the governance instrument for Anvil. If you are evaluating what is AMP coin in 2026, that distinction is essential.

“Collateral-as-a-Service”: Opening AMP to Any Financial Application

This is the alpha most competitors miss. While the docs do not always use the exact phrase, Anvil effectively turns collateral into a reusable service layer. Vaults hold approved assets, letters of credit reserve them, pools allocate them to claimants, and governance sets parameters such as token support, limits, and collateral factors. That is “Collateral-as-a-Service” in practice: other apps can plug into collateral infrastructure instead of building bespoke risk engines from scratch.

For AMP holders, that matters because the old “Flexa-only” thesis becomes too narrow. The long-term strategic idea is that collateral should become programmable middleware for payments, credit, bridging, deposits, and settlement assurance. AMP’s partition architecture and Anvil’s secured-credit primitives point in the same direction.

Scaling Beyond Retail: Institutional Use Cases for AMP in 2026

The institutional angle is not just theory. Official AMP docs already describe collateral for exchanges and margin relief, while Anvil docs explicitly mention counterparty credit, asset bridging, and layer-2 deposit or withdrawal assurance. That makes the AMP/Anvil stack relevant anywhere counterparties want immediate action before base-layer finality.

The Flexa Network

How Flexa Uses AMP Today

Flexa remains the clearest live demonstration of the AMP model. The company says merchants can accept 99+ digital assets with instant authorization, fraud resistance, and flexible payouts. In recent official releases, Flexa expanded Sheetz to all 750+ locations and launched with Bealls Inc. across more than 660 stores nationwide.

That matters because real merchant acceptance is where many crypto-payment narratives break down. AMP is still relevant because Flexa is not just theoretical settlement tech; it is deployed merchant infrastructure.

Why Merchants Prefer the Flexa/AMP Model

Flexa’s sales pitch is blunt: no chargebacks, no unexpected reversals, and guaranteed funds at the moment of payment. Compared with traditional rails, that is a huge operational difference for merchants who live with dispute risk, reserve holds, and delayed settlement.

SDKs and Integrations: Bringing AMP Collateral to Third-Party Apps

Flexa is also opening the front end. Its docs and newsroom describe SDKs for iOS, Android, and React Native, plus wallet-facing Components such as Spend and Scan. Zashi and Nighthawk integrations show how third-party apps can inherit Flexa’s merchant acceptance layer without rebuilding payments from zero.

The AMP Tokenomics: Supply, Staking, and Rewards

Staking AMP

Staking AMP means assigning your tokens to a collateral pool so they can underwrite payment activity. In return, stakers receive rewards. Flexa’s current v3 system adds time-weighted monthly reward distribution and predictable unlock windows, which is a meaningful upgrade over v2’s messier mechanics.

The Circular Economy

AMP’s original whitepaper described a straightforward flywheel: Flexa transaction revenue funds open-market AMP purchases, and those purchases are redistributed as network rewards. That means usage is supposed to feed demand for collateral and rewards simultaneously. The exact yield any staker sees still depends on pool choice, tenure, and network activity, but the economic loop is tied to actual transaction flow rather than arbitrary inflation.

Fixed Supply and Scarcity

Scarcity is part of the AMP thesis. CoinGecko lists AMP with a coded max supply of 100 billion and roughly 84 billion circulating, while Etherscan shows about 99.72 billion total supply onchain. That does not make AMP automatically “rare,” but it does mean holders are not underwriting an endlessly inflating collateral token.

Comparing AMP to Other Payment Protocols

AMP vs. Ripple (XRP)

XRP settles quickly, usually in a few seconds, and transaction costs are tiny. AMP’s edge is different: it is not trying to be the settlement asset itself, but the collateral that guarantees settlement across assets and apps. XRP gives you fast finality; AMP gives you asset-agnostic assurance.

AMP vs. Terra Classic (LUNC)

Terra Classic’s collapse turned one lesson into common sense: payment confidence built on reflexive design is fragile. AMP’s model is more conservative. It uses explicit collateral segregation, programmable controls, and partition-based accounting rather than algorithmic confidence. That is less flashy, but much more institution-friendly.

AMP vs. Traditional Rails (Visa/Mastercard)

Flexa says its merchant fee is 1%, lower than traditional card systems and some crypto processors. More importantly, it removes the chargeback logic that forces merchants to price fraud and disputes into everything else. That is why AMP is best seen as payments infrastructure, not just a speculative token.

| Network | Settlement Time | Transaction Fee | Fraud Protection Mechanism | Scalability |

| AMP / Flexa | Sub-second authorization; real-time merchant settlement | Flexa says 1% merchant fee | AMP collateral, escrow logic, no chargebacks | 99+ assets, 24/7 settlement, pool-based scaling |

| Visa | Typically 1–3 business days to merchant funding | Varies by processor and interchange; higher than Flexa’s 1% benchmark | Chargebacks, dispute management, network fraud tools | VisaNet capacity of 65,000+ transaction messages per second |

| Lightning Network | Near-instant | Usually tiny and route-dependent; nodes can charge base and forwarding fees | HTLCs and channel rules, but constrained by liquidity and routing | Off-chain scaling is strong, but path and channel liquidity matter |

| XRP Ledger | About 3–5 seconds | Minimum standard fee 0.00001 XRP | Ledger finality and consensus; no separate collateral backstop | 2000+ TPS / thousands settled in seconds |

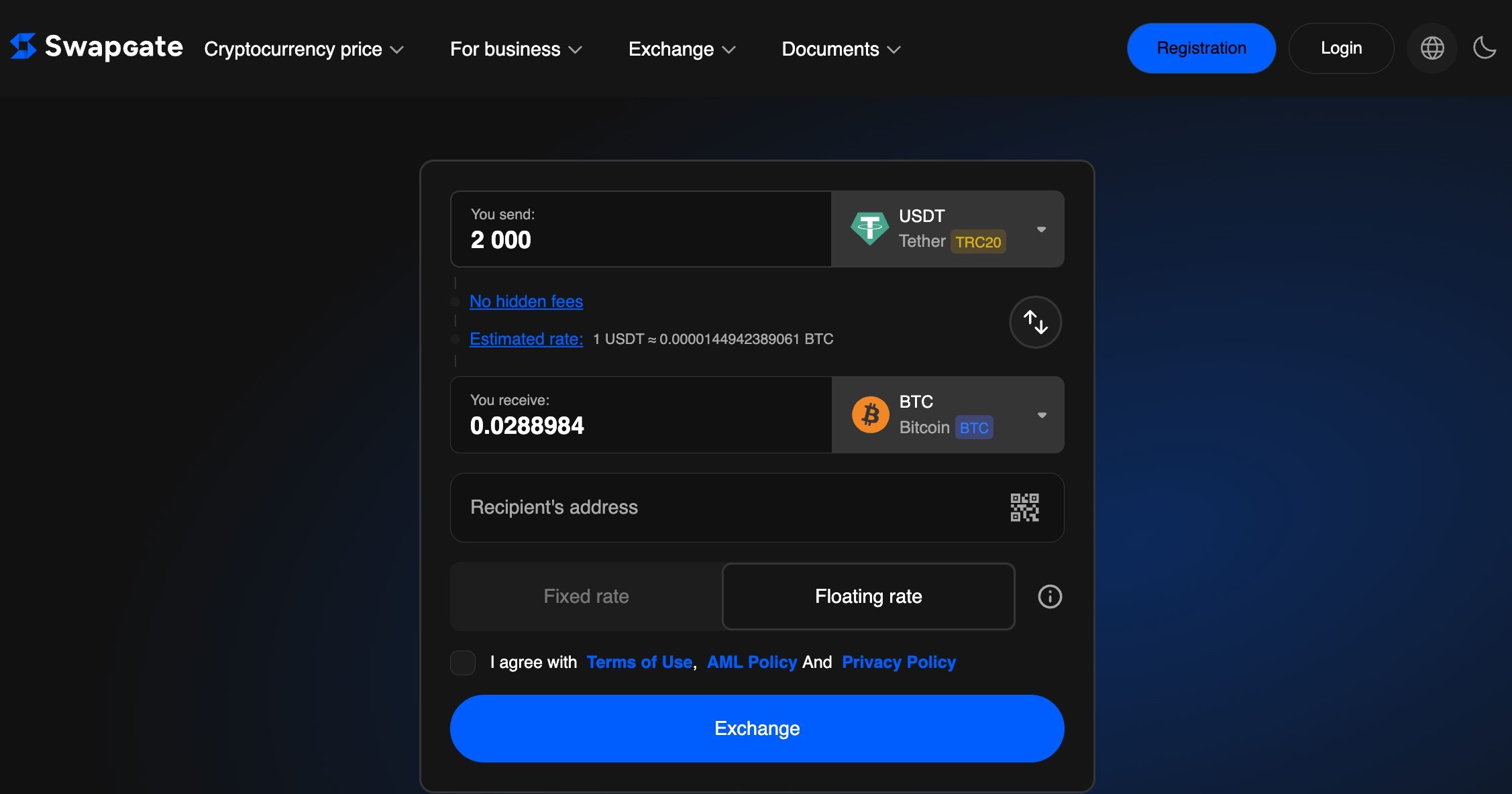

How to Buy and Exchange AMP Safely in 2026

SwapGate supports instant swaps, as for USDT to BTC, and dedicated exchange pages. If you use it, treat AMP as an Ethereum ERC-20 asset, confirm the contract address first, and send only to an ERC-20-compatible receiving wallet. Remember, the official AMP contract address is 0xff20817765cb7f73d4bde2e66e067e58d11095c2.

Best Wallets for AMP

Source: MetaMask

For storage, MetaMask and Ledger make sense because AMP is an ERC-20 token. MetaMask supports ETH-based tokens and lets users add custom ERC-20 contracts, while Ledger supports ERC-20 management through an Ethereum account. For spending rather than storage, Flexa-enabled wallet experiences such as Zashi and Nighthawk matter more because they connect into real merchant acceptance.

Regulatory Status and Security Audits

Is AMP a Security?

In the U.S., AMP’s status is still best described as unresolved rather than cleanly settled. The SEC named AMP among the crypto assets in its 2022 Wahi insider-trading complaint, and the case later reached final judgment against Sameer Ramani in 2024. But the AMP project itself was not a defendant in that case, and the SEC itself has acknowledged in outside commentary that many token projects were never parties able to contest those allegations directly.

Smart Contract Audits: Evaluating the Safety of the AMP Protocol

On the code side, AMP’s official docs say the token contract was audited by ConsenSys Diligence and Trail of Bits, with zero critical issues reported in both 2020 reviews. Anvil’s docs list later audits by OpenZeppelin and Trail of Bits, plus a 2025 OpenZeppelin diff audit tied to governance changes. That does not remove smart-contract risk, but it does show serious review coverage across both the legacy AMP layer and the newer Anvil stack.

The Decentralization Milestone

For Anvil at least, governance is now explicitly onchain. The protocol uses OpenZeppelin Governor contracts, and ANVL holders and delegates can set asset support, limits, and collateral factors. That is a meaningful decentralization milestone because collateral policy is no longer just a company decision; it becomes a community-controlled risk function.

Conclusion: Is AMP Still the King of Collateral?

- If you only view AMP through 2021 merchant-payment headlines, you will miss the point. In 2026, the interesting question is not whether AMP coin can “moon.” It is whether programmable collateral becomes a lasting layer in digital finance. If it does, AMP still has a real thesis.

- AMP remains relevant because it combines live merchant utility through Flexa with one of the more technically distinctive token designs in crypto: partitions, stake-in-place collateral, and manager-defined risk domains. The Anvil transition adds a second growth angle by extending the collateral story into secured credit and app-level financial infrastructure. That is why the best answer to what is AMP token in 2026 is not “a payment coin.” It is “a programmable collateral primitive.”

FAQ: Everything You Need to Know in 2026

What is AMP?

AMP is a universal digital collateral token used to guarantee any type of value transfer, from retail payments to institutional finance. By using smart contract partitions, it provides instant, fraud-proof settlement for the Flexa network and the broader Ampera ecosystem.

What is the difference between AMP and the new ANVIL token?

AMP is the collateral asset. ANVL is the governance token for the Anvil protocol. Flexa Capacity v3 still says it is powered by AMP, while Anvil docs say protocol operations are governed by ANVL holders through onchain governance.

Can I mine AMP tokens?

No. AMP is an ERC-20 token on Ethereum, so it is not mined like a proof-of-work coin. You typically acquire it by buying, swapping, or earning rewards through staking participation.

Which retailers currently accept payments via Flexa?

Examples confirmed in recent official Flexa releases include all 750+ Sheetz locations and more than 660 Bealls, Bealls Florida, and Home Centric stores. Flexa also says wallet integrations such as Zashi and Nighthawk enable spending at thousands of retail locations, so the exact experience depends on the wallet and merchant rollout.

Is it worth staking AMP if I only have a small amount?

It can be, but small holders should think about Ethereum gas costs and time horizon. Flexa v3 uses time-weighted monthly rewards and 12-to-24-hour unlock timing, so tiny balances may be less efficient unless you plan to hold long enough for rewards to outweigh transaction costs.